To say the markets have thrown a few curveballs the way of investors the last few months may be one of the larger understatements I could open this note with. Before diving into some better news, let’s take a stroll down the (recent) memory lane for a moment:

- Feb. 24th – Russia invades the Ukraine to start the largest European War since 1945

- March 1st – Oil rises above $100 p/ barrel for the first time since 2014 (CNBC)

- March 20th – 30 year mortgage rates eclipse 5% (google)

- The 2 – year treasury over the last 12 months rises from 0.16% to 2.85% (Thomson One)

- Relatedly, the Barclay’s Aggregate Bond Index gets off to the worst start on record (Barron’s)

- Expected number of Fed Rate hikes for 2022 goes from 2-3 in January to as many as 12 as of

the time of this writing (CBOE) - CPI continues its upward ascent reaching +8.5% year over year as of March 2022 (BLS)

Climbing the Wall

It is often said that bull markets climb a ‘wall of worry’. The list above certainly may feel as tall as a wall and have given investors plenty of worry.

However! Despite the headlines, volatility, and geo-political jitters, one sleepy corner of the investment markets performed admirably to start the year… that’s right you guessed it: Dividend Growth Stocks.

While bonds of all flavors (credit quality and maturity) struggled to reset to higher inflation and interest rates, and the growth heavy Nasdaq 100 saw losses of 8.91% in the first quarter, Dividend Growth stocks with their tendency to have strong pricing power, and presence in the materials, utilities, and energy sectors both cushioned drawdowns and outperformed to the upside in the quarter.

The S&P 500 had a peak-to-trough drawdown of 12.8% on a closing basis in Q1 (Yahoo finance). By comparison the Morningstar US Dividend Growth Index declined 9.6%. In fact, the higher yielding Dow Jones US Select Dividend Index saw positive returns in the quarter of +4.76%.

Unpacking the Resiliency

Beginning to unpack the “why” behind strong performance begins with pricing power. Unlike bonds where fixed interest rates are the norm or high growth stocks where current profits are often negligible, dividend growth stocks tend to have higher levels of current profits and the ability to raise prices while still receiving comparable levels demand.

We’ve seen this across the board from Oil companies to Soft Drink Manufacturers to Personal Goods and even Toilet Paper. The reaction to inflation has been to raise prices or ”pass through” rising costs to consumers. The net effect has been fairly stable profits margins, increasing revenues and fairly strong stock prices in the sector. After being left for dead in 2020 with negative oil prices, oil companies now find themselves the darling of the day making many times over the level of profits just a few years ago.

While the risk exposure is certainly different and there is no “return of principal at maturity” this pricing power component has the potential to make dividend growth equities a “better bond” in periods of rising interest rates and principal losses in traditional fixed income.

While Dividend stocks are by no means a “silver bullet” capable of conquering all headwinds the market throws at us, we continue to believe a collection of companies with current and growing profits, strong pricing power, quality balance sheets, and a commitment to financial discipline and returning capital to shareholders (via dividends & share buybacks) is a solid foundation on which to build a diversified portfolio.

The Seas Ahead

As always we are engaged in research on a variety of avenues to look on the horizon in an attempt to find returns and steer away from risk – detailed below are a few areas:

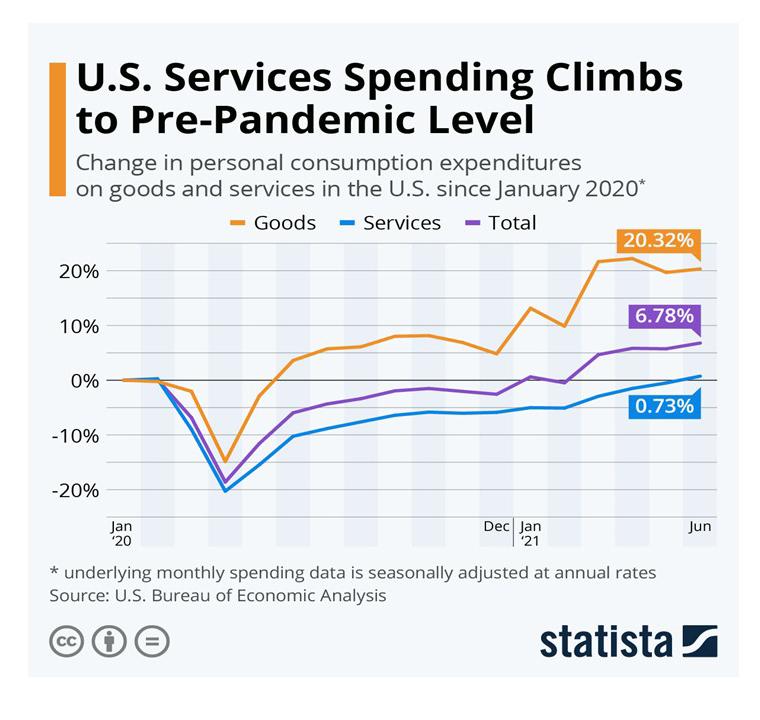

Goods vs. Services Spending

Goods vs. Services Spending

After several decades of a shift toward services, COVID saw massive increase in demand for hard goods (houses, cars, refrigerators etc..) We are anticipating a shift back to services as the remnants of the pandemic begin to fade.

Who’s investing?

Different than who’s investing in a given stock, we’re finding some of the most interesting opportunities based on what companies have the most opportunity to invest capital into their business. Companies with a track record of earning high returns from investments and what we believe to be a long run way to continue doing so make up some of our favorite areas including Industrial Gas infrastructure and Semiconductor equipment manufacturing.

What’s old is new again

Much like the oil saga referenced above, markets have a tendency to extrapolate both the best of news and the worst of news. On both ends we want to take a long-term view, particularly when it allows us to acquire quality companies at attractive dividend yields and potential growth rates.

Content in this material is for general information only and not intended to provide specific investment, tax, or legal advice or recommendations for any individual.

All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

Stock investing includes risks, including fluctuating prices and loss of principal.

Dividend payments are not guaranteed and may be reduced or eliminated at any time by the company.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

Morningstar US Dividend Growth Index is designed to provide exposure to U.S.-based securities with a history of uninterrupted dividend growth.

The Dow Jones U.S. Select Dividend Index aims to represent the U.S.’s leading stocks by dividend yield.

The Standard & Poor’s 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

April 2022