The nursey rhyme of Humpty Dumpty dates back to the 1800’s as a story of a character who climbs up and falls off a great wall, unfortunately incapable of being put back together again. As I began to prepare writing this note, I was struck by the fact that the daily headlines from Financial & Mainstreet media would suggest that American Companies and the stock market at large are facing the fate of Humpty Dumpty, and that should a recession hit, surely the companies would not be put back together again!

Embedded into the incessant discussion of “Hard” or “Soft” landing, is the idea that long-term assets (stocks) should fluctuate wildly in value, because of the near term outcomes of the economy.

HOWEVER! We think that this narrative discounts a couple of very important realities. Among them are two I want to highlight in this note. 1 – Not all companies are created equal and 2- American companies have faced greater tests over the last 20 years, by and large making the remaining firms stronger.

Not all companies created equal

In periods of volatility and economic weakness, there are a few factors that matter significantly to selecting companies for investment. Chiefly at the top of the list to me, is to what extent the company is reliant on “the kindness of strangers”. The kindness of strangers is a euphemism authored by Warren Buffett to describe companies that need access to the stock or bond markets to raise capital to fund their business. Instead of kindness, the companies we prefer within our Dividend Strategies tend to be indifferent to the capital landscape.

Clearly, most business owners prefer a world of high growth, strong demand, moderately low unemployment, and minimal inflation, however companies with strong balance sheets and time tested pricing power in their markets are better built to withstand the vicissitudes of the economy and capital markets. Importantly, dividend growth in and of itself doesn’t mean a company is strong but it has shown to us to be an excellent signal and starting point for our research process.

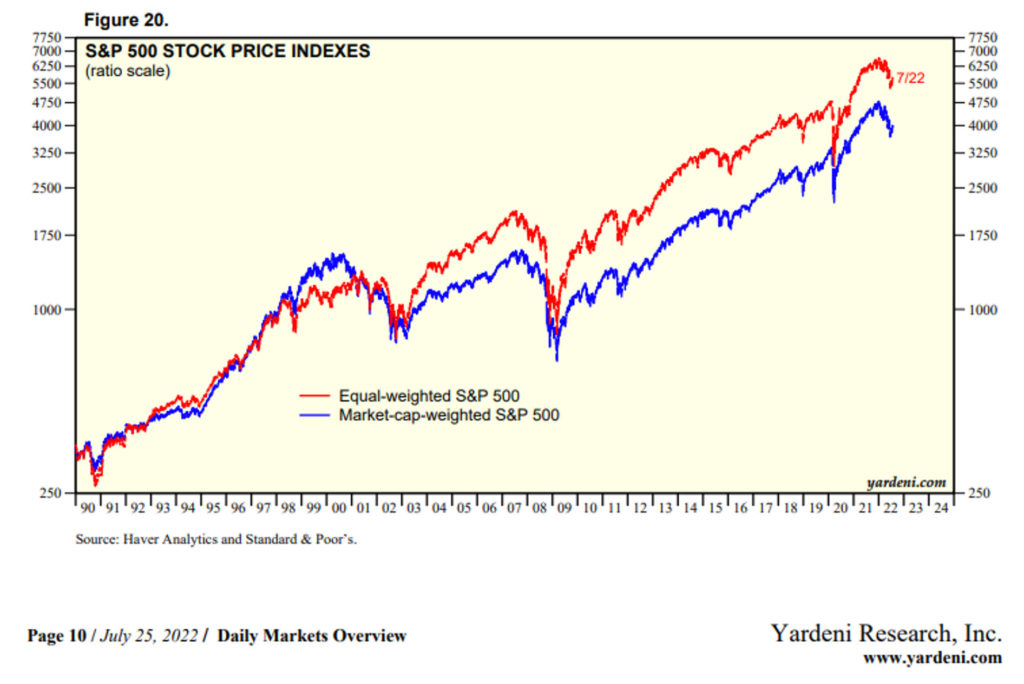

Within our research process, we by no means want to discount the role of innovation and “big ideas” or their ability to create immense value, but with a forced commitment to profitability, we have avoided some of the largest potholes in the financial markets this year. Putting numbers to this, for the first six months of the year, the Morningstar US Dividend Growth benchmark returned -13.55%, while the S&P 500 was down -19.96% and the Nasdaq 100 (Tech heavy) Index was down -29.22%.

The tests of the last 20 years

Dot Com mania, 9/11, The Accounting scandals of Enron and Worldcom, The Great Financial Crisis, Greek Debt Default Fears, Oil Price Crises in 2015, Brexit, The largest pandemic in a century, and the highest inflation in 50 years… ALL of this has happened in the last roughly 20 years. All have been “thoughtful reasons” to not invest, or at the least provided corporate executives and business owners challenging operating environment. Despite all of these, the drumbeat of progress has continued, profits and dividends have grown, the strong have separated from the weak, and markets have generated handsome returns for the patient investor. We have no reason to believe this time will be different, albeit nothing is guaranteed.

So far this year, we have been fairly active in the portfolios, focusing on opportunities we believe will increase the portfolio weighted yield, future dividend growth rate, or in a perfect world, do both at the same time. We remain diversified by sector and industry, and are pleased that once again this year no companies have cut a dividend.

Given the amount of market participants that remain focused on “flipping” stocks versus owning businesses, we don’t expect market volatility to calm down until inflation makes a persistent move lower (potentially underway with gas prices this month) and the Federal Reserve gains cover to halt increasing the Fed Funds Interest Rate. As such, we do retain what we consider to be a good bit of dry powder to initiate or increase positions in the best businesses as opportunity increases.

Nevertheless, we believe that companies with products that generate positive and growing cash flows of which they distribute a growing amount to shareholders will perform well in the coming weeks, months, and years, and it is to the end of identifying and investing in the these companies that we work.

August 2022

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. All investing involves risk including loss of principal. No strategy assures success or protects against loss.

Dividend payments are not guaranteed and may be reduced or eliminated at any time by the company.

The Standard & Poor’s 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.