As you have heard us say over the years, we believe Dividend Growth investing to be a key anchor of a diversified investment portfolio. Particularly in the low interest rate environment of the past decade, dividends provide cash flow that can either be spent, kept in cash, or reinvested into additional shares of stock. This cash flow also has historically served as a “buffer” to stock market volatility as dividends tend to be much more stable than earnings or share buybacks over time. Additionally, with interest rates and bond yields historically low, the potential for a growing income through dividend stocks has been a compelling option for investors. This note will touch on aspects of why we continue to believe the strategy makes sense in today’s market environment, as well as a few notable items from 2021.

Overall, 2021 was a great year for US stocks with the S&P 500 returning 26.9% for the year (CNBC). Dividend stocks tracked just behind that number with the Spliced S&P U.S. Dividend Growers Index returning 23.7% in the year (Vanguard). At the end of 2021, 78% of the companies in the S&P 500 were paying a dividend (ETF.com). Importantly, we use a process in our portfolios to only invest in companies that have demonstrated an ability to pay a growing dividend through both the ups and downs of the economic cycle. Right now, our “screens” narrow the universe from the nearly 6,000 listed stocks in the US (market watch) down to about 200 companies to consider for inclusion in our portfolios.

Handing the baton from a strong 2021, 2022 has thus far been bumpy to say the least, as a decelerating economy (slower growth), rising interest rates, growing inflation, and geo-political complexities led to the first 10% drawdown in the S&P 500 in over a year. Dividend Stocks, particularly those in the areas of Consumer Staples held up very well in this environment, whereas growth stocks have seen steeper losses (Thomson One).

Level setting the past, let’s turn to the future. We see a variety of narratives in the market that may keep volatility higher for a period of time, but we do not believe the best days are behind us, and instead that these narratives will build the “wall of worry” that a growing economic and corporate sector can overcome in the future.

Supply Chains

Supply Chains have been front and center for over 6 months now. The reality is time heals wounds, and the supply chain is improving. Comments from Apple, AMD, and others indicate things are mostly getting better. Q4 inventories as a part of GDP saw significant growth. This means we may see lead times drop and shelves get re-stocked in the coming weeks and months.

Two Way Risks Re-Emerge

Since April 2020, while COVID and its related economic false starts have been a constant presence in markets, the active presence of the Federal Reserve, from buying corporate bonds, to Quantitative Easing, and 0% short term interest rates, led to a market that mostly had “1-way risk”. This is because investors had one side where the economy performed well, and the other where the Fed and even Congress were ready and able to jump in with stimulus if road blocks emerged. This dynamic created a market where investors lagged indices more by not being aggressive enough than they did by taking too much risk. Examples of this behavior can be seen across the landscape from the GameStop phenomenon to the rabid demand for new IPO’s and the onset of SPAC-mania. Late 2021 into 2022 is beginning a new chapter in our minds where two-way risks matter again. Inflation is high and the Fed is likely to become less accommodative (raise interest rates & end QE) rather than more. This is healthy in our view and doesn’t make us overly concerned, but does explain why a pick-up in volatility and widening corporate credit spreads is taking place. Importantly, “two-way risks” does not mean “only downside”, just that the market will likely have to carry its own weight over the course of the next year or two.

Economic Growth & The Labor Force

Q4 GDP growth was very strong with real GDP up +6.9% in the quarter. Our outlook is that while the first quarter may be soft, 2022 should be a strong year once again of above-trend (3-4%) growth. However, one measure of the economy that has not regained its former glory is the Labor Participation Rate. As you’ll see in the below chart, we’re still about 1.2% below the pre-covid participation rate. While there are a litany of possible explanations, we expect that a more positive COVID backdrop in 2022, higher volatility in Stock and Crypto markets, and higher wages, could lead a meaningful number of people back into the workforce this year.

Where do we go from here?

There are a litany of other factors that we could add to this “wall of worry”, including a certain East European leader that seems bent to invade its pro-democratic neighbor, but in spite of all of these factors, we believe the market can climb the “wall of worry” powered by continued growth in corporate earnings and the US domestic economy.

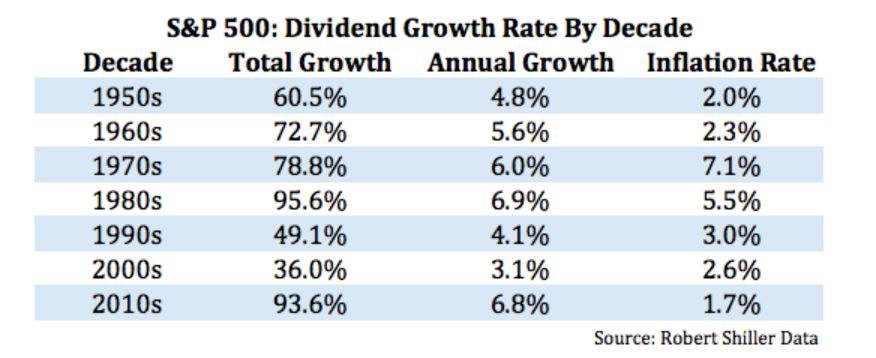

Importantly, there is no strategy that can prevent every drop in stock prices while retaining the upside of good growth, but the purpose of an “all-weather” strategy like dividend growth is that while stock prices will fluctuate (sometime significantly so!), we believe this strategy as part of a broadly-diversified portfolio maximizes the likelihood of growing your portfolio on a real (net of inflation) basis over time. Highlighted below is a chart we provided in last quarter’s letter showing the growth of dividends in the S&P 500 vs inflation over time.

We have had several companies already announce increases to their dividends this year, and S&P 500 earnings are projected to be up 9% in 2022 (FactSet), this is a positive backdrop for long-term owners of diversified stock portfolios.

Thank you for the opportunity to serve as your experienced advisor and please let us know if you’d like to have a conversation about this portfolio or anything else.

Q4 2021