With the air beginning to get a little more crisp, and holidays just around the quarter, we wanted to provide you with an update on our Dividend focused individual stock portfolios as we enter the closing stretch of 2021.

At a high level, markets finished the third quarter (September 30) little changed from the previous as solid returns across US.

Stocks in July and August were given up during the month of September as the S&P 500 had its first 5% correction since early November of 2020. The Morningstar Dividend Index posted a return for the third quarter of -0.25%.

Nevertheless, markets have reversed course higher to start the month of October as corporate earnings season has kicked off and initial results have once again been strong adding conviction to our view that it is likely we see reasonably strong growth over the next 18 to 24 months in corporate earnings and the economy.

Despite this strong earnings backdrop, one item that has been talked about with increasing frequency has been the concern of inflation remaining higher for longer. While somewhat artificially high given low prices a year ago, The Labor Department announced September CPI (broad measure for inflation) increased 5.4% from a year earlier, eliminating volatile food and energy the index was up 4.0% year of year (US Bureau of Labor Statistics).

With inflation expected to remain above 2% over the next one or two years, this has made investing in fixed income more difficult as some areas appear destined to lose money on a “real” or “net of inflation” basis. With savings accounts and Bank CD’s offering paltry returns as well, this has made income investing a difficult landscape.

One area where we are still finding opportunity however is in Dividend Growth Stocks. The reason for this lies in the strategy, which is to identify business that we believe have the ability to grow revenues, profits, and dividends year after year. In fact, some businesses actually see stronger dividend growth in periods of inflation as they are able to increase their prices at a faster rate. Some of the businesses we invest in across financials, industrials, and materials are currently experiencing these benefits.

A key element of our process over the past few quarters has been to analyze the strength of our portfolio companies to “pass through” cost increases in their business to the end consumer. Our research has identified strength across many of our industrials, materials, and financials businesses confirmed by what has been a good start to earnings season mentioned above.

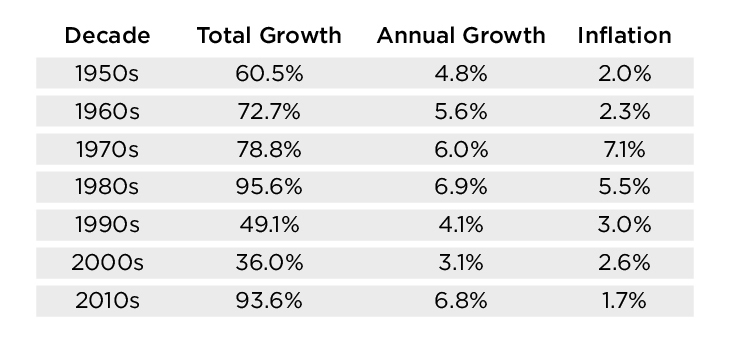

Underscoring the power of dividends, we have included a chart below highlighting the persistence of dividend growth across US stocks through 2015 (S&P500), showing that across the decades, there has only been one period of below inflation rate growth. (source: awealthofcommonsense.com)

S&P 500: Dividend Growth Rate By Decade

We do not forecast inflation averaging 5, 6, or 7% over the next 3 to 5 years like that seen throughout the 1970’s and 80’s, and as a result we believe Dividend Growth Stocks have the potential to be an important piece of a diversified portfolio; adding an income stream with the potential to keep up with and beat inflation over time.

Finally, as we have mentioned in previous letters an important part of our process is listening to portfolio companies earnings calls (led on our team by Dr. Lyle Bowlin). Included below are a few of the headlines that we found the most notable over the last quarter.

KLA Tencor Raises Dividend 17% and announces additional $2 Billion Share Buyback

Air Products Announces Price Increases of 15-20%

“Consumers are spending 20% more than before the Pandemic” – Jamie Dimon, CEO JPMorgan Chase