With higher interest rates, what role do dividends and dividend growth investing play in a portfolio?

For many years after the Financial Crisis, it was common for the yields available from dividend stocks to exceed the paltry interest rates available from banks, money markets, or US Treasuries. Taking advantage of this higher income proved profitable for investors as the Morningstar US Dividend Growth Index returned an annualized return of 10.26% for the 5 years ending 12/31/2022.

The case for dividend stocks today is a bit more nuanced. With interest rates rising dramatically, there are few stocks with yields matching the 5.5% Fed Funds Rate. Does that mean investors should shun dividend stocks at this point?

We don’t think so.

While we are generally in favor of playing defense in today’s markets and like short-term treasuries as a tactical position, Treasuries or Bank CD’s carry two main downsides:

- Short Term Fixed Income doesn’t have meaningful potential for capital appreciation or growth of income.

- Short Term Fixed Income can contain high “Reinvestment Rate Risk” if the client’s goals are predominantly long-term while the investment is only locked in for a short-term period.

Growth of Income

When looking at an investment one of the easiest metrics to find is the starting yield, however that only tells part of the story. In reality, the time horizon for many of our goals are likely 5, 10, 20, or even 30 years in duration. This means we need to evaluate the growth of income for our investments as well as the starting level.

This concept in Dividend Investing is known as “Yield on Cost”. For example, if you invested $1,000,000 at a starting dividend yield of 2.5%, you’d start with $25,000 a year in dividends. Meanwhile a bond yielding 5% would be paying $50,000 in interest. While the dividends start at ½ the amount of the bond, over the past 10 years the S&P 500 has seen dividend growth of approximately 8% per year (Yahoo Finance). At that growth rate, the dividend income of the portfolio doubles every 9 years. So, for long-term goals stretching to 20-30 years, it would not be uncommon for the initial dividend income of $25,000 to grow to $100,000 to $200,000 over the long-term.

Reinvestment Rate Risk

Reinvestment Rate Risk is defined as the chance an investment will generate lower than expected income due to a future drop in interest rates. While this risk can often be “invisible” to investors, we encounter it every day when talking to clients. Consider this example:

- Would you rather invest in a 10-year bond yielding 4%, or a 1 year bond yielding 5%.

Your initial reaction is likely to lean towards the 1 year bond as a shorter investment feels less risky and carries a higher rate, but truly the correct answer is: It depends on the duration of your goals (and the path of interest rates).

If you have long-term goals OR interest rates begin to come down, you’ll likely be better off with the 10-year strategy.

The exact same idea holds for Dividend Paying stocks. Generally, stocks are considered “Long Duration” as they never mature and entitle the owner to a share of all future corporate profits, and as a result they are often a strong strategy to consider for funding long-term goals.

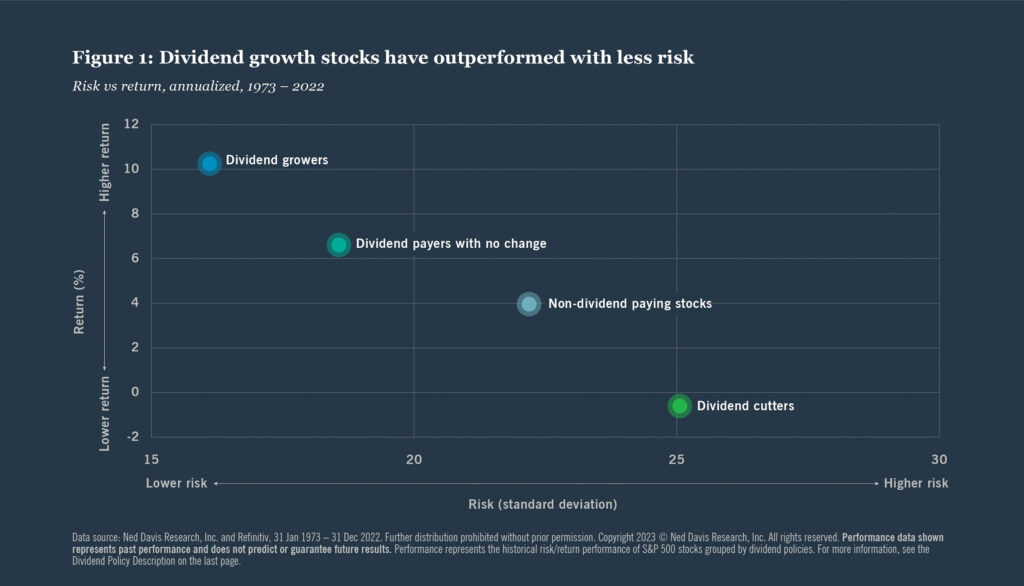

Finally, in addition to the discussion above, it’s also important to highlight that historically companies that grow their dividend perform very well in terms of price appreciation as well. Below is a chart from Nuveen and Ned Davis Research showing the outperformance of companies that pay a growing dividend.

We think fixed income and treasuries are very attractive in this environment, but its important not to go too far in chasing these higher yields. Stocks & business ownership have historically been the largest long-term generators of wealth known to man, and we don’t expect that to change any time soon.

We think fixed income and treasuries are very attractive in this environment, but its important not to go too far in chasing these higher yields. Stocks & business ownership have historically been the largest long-term generators of wealth known to man, and we don’t expect that to change any time soon.

The markets are an ever-changing organism, and we remain steadfast in our efforts to identify the best dividend growth opportunities of today and tomorrow in addition to our other investment strategies and comprehensive financial planning. It is to these ends that we work.

September 2023

Dividend payments are not guaranteed and may be reduced or eliminated at any time by any company.